The post Ballards LLP Celebrating Double Award Shortlisting appeared first on AGN International.

]]>The dual recognition highlights Ballards LLP’s exceptional performance across multiple disciplines and reinforces the firm’s position as a progressive leader in the accountancy sector.

Mid-Tier Firm Excellence

The Mid-Tier Firm of the Year category recognises firms with a fee income of between £2m-£10m that demonstrate exceptional specialist strategy and defining qualities in a highly competitive market. Ballards LLP’s shortlisting reflects the firm’s robust multi-team structure, strategic approach to client service, and consistent delivery of measurable results across its operations.

“This recognition validates our commitment to delivering exceptional value to our clients whilst maintaining the highest professional standards,” said James Syree, CEO and Partner at Ballards LLP. “Our success is built on our specialist expertise, strong client relationships, and our dedicated team’s unwavering focus on excellence.”

Leading Progressive Audit Practice

The firm’s nomination for Audit Firm of the Year acknowledges Ballards LLP’s progressive approach to audit quality and innovation during a period of significant regulatory change. This category celebrates firms that demonstrate exceptional culture, leadership, and commitment to audit quality whilst embracing new regulations and methodologies.

Ballards LLP has distinguished itself through its investment in cutting-edge audit technology, comprehensive staff development programmes, and robust quality assurance frameworks that consistently deliver high-quality audits serving public and stakeholder interests.

“At a time when the audit profession faces unprecedented challenges, we’ve embraced change as an opportunity to strengthen our practice,” explained Ben Powell, Audit Partner at Ballards LLP. “Our focus on innovation, quality, and staff engagement has enabled us to not only meet but exceed the evolving expectations of our clients and regulatory bodies.”

Building on Success

The shortlisting comes as Ballards LLP continues to expand its influence across the Midlands region, with the firm consistently demonstrating strong client retention rates, enhanced profitability, and positive feedback from clients who value the firm’s proactive approach and technical expertise.

The firm’s commitment to professional development has also led to exceptional staff retention and engagement levels, fostering a collaborative culture that drives continuous improvement and innovation.

Awards Recognition

The Accounting Excellence Awards celebrate outstanding achievement across the accountancy profession, recognising firms that demonstrate exceptional quality, innovation, and client service. The winners will be announced at the awards ceremony on September 30th, 2025.

“Being shortlisted alongside such distinguished firms is a tremendous honour,” added James Syree. “This recognition reflects the collective efforts of our entire team and reinforces our commitment to setting the standard for excellence in the Midlands accountancy sector.”

About Ballards LLP

Ballards LLP is a progressive Midlands-based accountancy firm providing comprehensive audit, tax, and advisory services to businesses and individuals across the region. With a commitment to innovation, quality, and exceptional client service, the firm has established itself as a trusted partner for organisations seeking expert financial guidance and support.

Head Office

Oakmoore Court

Kingswood Road

Hampton Lovett

Droitwich

WR9 7TD

ENGLAND

Contact Form

Tel: 01905 794504

Web: https://ballardsllp.com/

The post Ballards LLP Celebrating Double Award Shortlisting appeared first on AGN International.

]]>The post Unlocking Business Insights: How Audits Can Reveal Hidden Opportunities appeared first on AGN International.

]]>The term “audit” for many businesses brings to mind regulatory scrutiny, along with compliance requirements and administrative challenges. However, this view misses a crucial point. A properly conducted audit represents more than a mere regulatory requirement because it serves as a strategic instrument that reveals operational weaknesses while enhancing control systems and detecting potential areas for business expansion.

Audits become effective tools for business enhancement when conducted by knowledgeable professionals with a clear purpose, as they reveal both operational and financial aspects, which lead to better performance and sustained success.

Beyond Compliance: The True Value of an Audit

Audits are primarily driven by financial reporting obligations and regulatory standards, yet they consistently yield numerous hidden insights during the process. Through independent and objective assessment, an exhaustive audit evaluates a company’s financial condition as well as its control systems and operational integrity. An external viewpoint helps to identify operational trends and risks alongside hidden inefficiencies that normal operations fail to detect.

Some of the critical benefits include:

- Identifying inefficiencies in operations or cash flow.

- The audit identifies areas where control systems show weaknesses or inconsistent application.

- Assessing both the correctness of financial information and the trustworthiness of data used for making business decisions.

- Detecting unrecognised risks or liabilities.

- Revealing underperforming business units or unprofitable products.

- Finding potential tax and compliance problems before they develop into bigger issues.

Businesses that engage with audit processes move beyond compliance to establish stronger positions for strategic decision-making and resource optimisation while planning growth.

Calibre Business Advisory’s Role in Adding Value

Growing businesses with limited internal staff or disjointed financial structures often find the audit process challenging to navigate. Calibre Business Advisory can assist businesses during this stage of the process. Organisations work with Calibre to transform their audit outlook from a burdensome necessity into a strategic advantage through our deep expertise in audit preparation and advisory services.

Their approach involves:

1. Pre-Audit Readiness and Risk Assessment

Calibre collaborates with clients to evaluate financial records and risk exposures as well as internal control status before starting the audit process. The process promotes efficient auditing alongside early detection of warning signs.

2. Liaising With External Auditors

We function as a connecting point between the business and external auditors while managing documentation completeness and response accuracy, and explaining potential issues. The process enhances engagement while minimising unexpected risks.

3. Translating Audit Findings Into Strategic Insights

Calibre provides advisory services immediately after the conclusion of many audit reports. Our experts translate audit findings into business strategies by pinpointing internal inefficiencies, procedural gaps, and financial inconsistencies that need resolution.

4. Embedding Continuous Improvement

Calibre inspires clients to move beyond the perception of audits as annual activities by fostering a year-round culture of continuous improvement using audit insights to boost operational performance, compliance standards and strategic growth planning.

Case in Point: Operational Efficiency

Audits often reveal critical insights about operational inefficiencies, which hold significant value. Operational inefficiencies can appear as poor inventory management systems alongside ineffective procurement procedures and repeated administrative operations with insufficient cost tracking methods. Businesses that discover inefficiencies can create better processes which help cut waste, increase profit margins and use resources more efficiently.

Calibre’s team provides clients with customised action plans to execute audit recommendations, which include tasks such as software integration, workflow restructuring and staff retraining. Businesses achieve better audit compliance along with improved business agility and cost savings.

Strengthening Internal Controls and Governance

The implementation of robust internal controls plays a key role in reducing fraud risk while guaranteeing data integrity and sustaining stakeholder trust. The audit process consistently identifies system weaknesses, including insufficient separation of duties, together with undocumented policies and unrestricted access to financial information.

Businesses can establish risk-based control frameworks matched to their organisation’s size and complexity through collaboration with Calibre Business Advisory. Control frameworks can involve automated approval workflows as well as delegated authority matrices, together with enhanced reporting tools. Better governance helps organisations succeed in audits while also establishing long-term stability and building investor trust.

Leveraging Financial Insights for Strategic Growth

Financial audit results expose underlying trends, including weak business segments and irregular revenue patterns alongside unnecessary spending areas. These insights act as a foundational platform to develop strategic plans.

For example, a business might:

- Streamline product offerings based on margin analysis.

- Adjust pricing strategies to improve profitability.

- Divest underperforming assets.

- Reinvest in high-growth areas.

Businesses that utilise these insights together with professional advice from business advisors can achieve decisions that maintain financial stability and capitalise on market opportunities.

Aligning with Evolving Regulatory Expectations

The regulatory sector has recently placed greater emphasis on ESG (environmental, social, and governance) disclosures, cyber risk mitigation, and corporate transparency standards. Modern audits now cover expanded areas, which makes remaining proactive crucial for businesses.

Sydney-based audit firms, including Calibre’s partners, maintain up-to-date knowledge of current reporting standards and industry expectations. Businesses that maintain compliance while demonstrating proactive governance build a stronger reputation that attracts stakeholders, customers and investors.

Embedding a Culture of Continuous Review

A shift in mindset represents the most powerful legacy that results from a high-impact audit. Companies that approach audits simply as compliance exercises fail to realise opportunities for ongoing enhancement. Organisations that adopt the review and reflection process as part of their operations obtain a strategic advantage.

Audits as a Catalyst for Growth

An effective audit process has the power to act as a transformative force within businesses rather than being just a formality. Audits empower organisations to eliminate hidden weaknesses and financial misunderstandings while directing them toward operational an improvement, which enables them to solidify their core structure and capitalise on growth possibilities.

Businesses achieve maximum audit benefits when they partner with established professionals from organisations like Calibre Business Advisory. Audits transform from mere compliance tasks into vital instruments for sustained success through custom support and strategic execution.

Audit services in Sydney are a wise investment for businesses that want to access these growth opportunities. Organisations that combine curiosity with thorough preparation and a dedication to continual betterment during audits can improve their performance while establishing trust and succeeding in complex global environments.

Contributed by:

Calibre Business Advisory

Level 8, 1 York St Sydney NSW 200

Web: https://calibreba.com.au/

Email: enquiries@calibreba.com.au

Phone: +61 2 9261 2177

The post Unlocking Business Insights: How Audits Can Reveal Hidden Opportunities appeared first on AGN International.

]]>The post Press Release: JRD Hosts the 2025 AGN German-Speaking Meeting in Warsaw, Poland appeared first on AGN International.

]]>A Warm Welcome to Warsaw

The meeting began on Thursday evening with a relaxed networking cruise along the Vistula River, offering attendees panoramic views of the Warsaw skyline in summer light. The friendly atmosphere was immediately evident, with many participants reconnecting after some time apart. The informal setting helped to ease into meaningful conversations and re-establish personal connections – a hallmark of AGN events.

Focused and Forward-Looking: The Technical Program

Friday featured a full day of technical sessions tailored to current challenges and opportunities in cross-border professional practice. Topics included:

- Insuring tax risk

- Exit tax regulations across EU jurisdictions

- The ESG Act: current legal status and implementation

- Setting up a subsidiary in Poland and comparative EU holding structures

- VAT treatment of e-commerce transactions and the legal framework for implementing VIDA

The day opened with a video address from AGN CEO Malcolm Ward, who provided a strategic update on the organisation’s global priorities and member initiatives.

A Cultural and Collaborative Experience

On Friday evening, attendees visited the historic Koneser Vodka Distillery, where they enjoyed a guided tour, tasting experience, and a short film produced by JRD Tax exclusively for the event. The program also included a talk on the Polish economy, a themed quiz, and a formal dinner at one of Warsaw’s top restaurants – an ideal setting for continued discussion and camaraderie.

On Saturday, those remaining took part in a guided tour of Warsaw’s Old Town, with time to explore its heritage sites and charming local streets. The cultural program added a deeper appreciation for the city and gave members more space to connect beyond the meeting room.

Shared Purpose and Lasting Value

The organisers extend their sincere thanks to all who participated, noting the high level of engagement, openness, and expertise shared across the weekend. The event reflected AGN’s ongoing commitment to building strong professional relationships, staying ahead of technical developments, and embracing the distinctiveness of its members.

Participant Reflections

“Tomasz and his team at JRD did a great job hosting the German-speaking meeting of AGN in Warsaw. Great content, excellent speakers – and best of all, you felt the heart of the great people of Poland. It felt like home to me. Looking forward to our next exchange.”

— André Marius Le Prince, Partner, WLP GmbH, Hamburg

The post Press Release: JRD Hosts the 2025 AGN German-Speaking Meeting in Warsaw, Poland appeared first on AGN International.

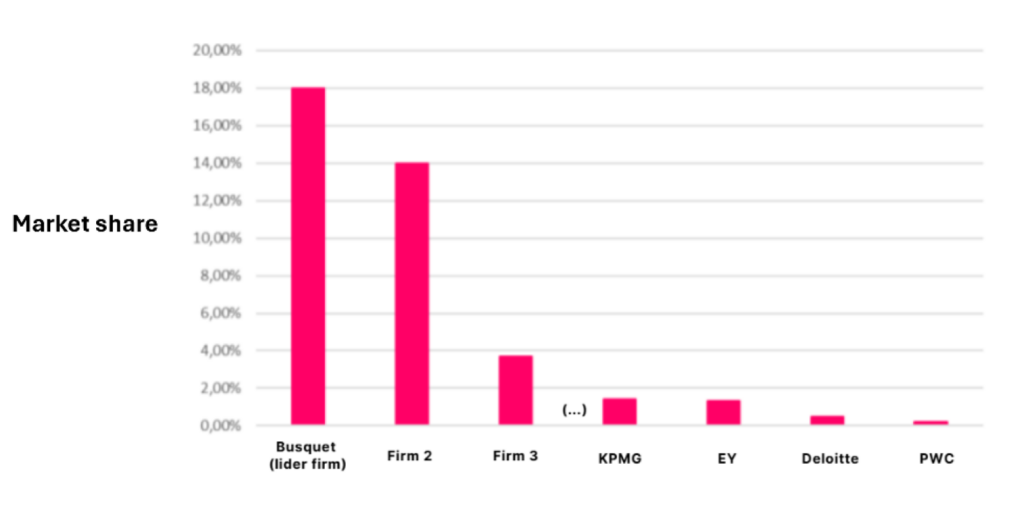

]]>The post Busquet Economistas Auditores is recognised as the Leading Firm in the Non-Profit Sector Audit Market in Spain appeared first on AGN International.

]]>Non-profit organisations play an essential role in society, especially in contexts where public institutions often fail to meet all social needs. These organisations act as key pillars of solidarity and social justice, addressing diverse issues such as human rights protection, poverty alleviation, cultural promotion, environmental protection, and support for vulnerable groups.

These organisations’ agility and flexibility make them key actors in responding to emergencies or social vulnerabilities, areas where public sector bureaucracy or limited resources cannot always reach. However, this operational autonomy also presents a challenge: ensuring effective, transparent, and responsible management of the funds received, which is particularly relevant in a context where a significant portion of resources comes from donations and grants.

A Sector with Specific Audit Needs

Auditing in the non-profit sector differs from other economic areas due to its particularities. Public trust in these organisations largely depends on their ability to manage resources clearly and efficiently. Busquet Economistas Auditores understand the specific requirements of this sector, which has enabled them to become the leading reference in non-profit auditing in Spain.

The main challenges in auditing non-profit organisations include:

- Management of donated resources: Non-profit entities manage funds that mainly come from donations and public grants, which require transparent use to ensure that commitments made to donors are fulfilled.

- Public trust: Clarity in fund management and proper use of resources builds public trust, essential for maintaining the organisation’s reputation and stakeholder support.

- Fraud prevention: Rigorous audits reduce the risk of misappropriation of funds and ensure the prevention of fraudulent practices, protecting both the organization and its beneficiaries.

- Compliance with regulations: Non-profit organisations are subject to specific regulations that require transparent administration and accountability to the relevant authorities.

- Accountability: Transparency and accountability are essential to demonstrate that the resources managed by these entities are used appropriately and in line with the social causes they promote.

Commitment to Leadership and Excellence

Being the leading firm in non-profit auditing involves a great responsibility for Busquet Economistas Auditores. Their work ensures proper fund management and reinforces public trust in a sector that plays a fundamental role in society.

Busquet Economistas Auditores remains committed to continuous improvement in the sector, promoting transparency and helping non-profit organisations optimise their management processes so that they can continue generating a positive impact in the lives of people and vulnerable communities.

Appendix 1:

Busquet Economistas Auditores

Via Augusta, 343

08017, BARCELONA

Contact Form

Tel: 93 414 71 83

Web: https://www.busquet.com/es

The post Busquet Economistas Auditores is recognised as the Leading Firm in the Non-Profit Sector Audit Market in Spain appeared first on AGN International.

]]>The post Press Release: AGN International Hosts Successful Excellent+NextGen Event: Building the Future of Leadership and Collaboration appeared first on AGN International.

]]>Held in a dynamic and interactive setting, the event was designed to equip the next generation of leaders with the tools and knowledge needed to excel in an evolving business landscape. Participants left inspired, empowered, and ready to embrace the future.

AGN 2024 Excellent+NextGen – Day 1: Developing Leadership through Advanced Presentation Skills

The first day of the event, Thursday, November 28, was dedicated to personal and professional growth. The day featured an engaging Advanced Presentation Skills workshop led by Nexia’s Head of Learning and Development, Alastair McTavish. This hands-on workshop focused on cultivating essential soft skills, including public speaking and audience engagement.

“The presentation skills workshop pushed me and no doubt others out of our comfort zone as it was very interactive, requiring us to practice in small groups that continuously mixed up throughout. Once I overcame my initial nerves, it was beneficial and a brilliant way to meet so many other attendees. The top tips I took away were learning gestures and voice variations to help speak with more impact and planning and structuring more effectively.”

Charles Wiltshire ACCA, Audit Senior at Dafferns LLP

The day stimulated confidence, camaraderie, and communication skills essential for effective leadership.

AGN 2024 Excellent+NextGen – Day 2: Exploring Global Tax and Audit Challenges

The second day, Friday, November 29, offered a deep dive into key tax and audit topics. Experts from AGN and Nexia shared updates on technical standards and the latest regulatory developments, fostering a collaborative exchange of global perspectives.

Highlights from the day included:

- OECD Updates: Florian Fuchs (AGN) delivered an introduction to global developments, followed by discussions on permanent establishments featuring professionals from Germany, Poland, the Netherlands, Switzerland, France, and the USA.

- VAT in a Digital Age: Iain Masterton (AGN) and Nick Hart (Nexia Saffery) presented on the evolving VAT landscape, outlining upcoming changes from 2025-2030.

- AI and Efficiency in Professional Services: Christophe Sauthon (Nexia S&A) captivated attendees with a session on leveraging AI and generative AI tools like Microsoft Copilot for increased efficiency and innovation.

The event also featured a joint session led by Malcolm Ward (AGN CEO) and Paul Ginman (Nexia Interim Chief Executive), emphasising the importance of the collaborative alliance between AGN and Nexia.

Looking Ahead

The Excellent+NextGen event exemplifies AGN International’s commitment to supporting AGN firms’ talent and emerging leaders and facilitating collaboration. As AGN members navigate an increasingly interconnected world, these opportunities to engage, learn, and innovate together are invaluable.

About AGN International

AGN International is a worldwide association of separate and independent accounting and advisory businesses. With nearly 200 member firms in over 80 countries, AGN connects professionals and clients globally to share expertise and best practices.

For more information about AGN International or the Excellent+NextGen event, visit my.agn.org.

The post Press Release: AGN International Hosts Successful Excellent+NextGen Event: Building the Future of Leadership and Collaboration appeared first on AGN International.

]]>The post Press Release: Aeberli Treuhand AG Hosts Successful German-Speaking AGN Meeting in Zurich, Switzerland appeared first on AGN International.

]]>Welcoming AGN Friends and Colleagues to Zurich

The event commenced on Thursday evening with a traditional Swiss aperitif at the AEBERLI LOUNGE, which had been thoughtfully transformed into a cozy Swiss Fondue Chalet. There, guests enjoyed authentic Swiss cheese fondue and other traditional dishes, setting the stage for a warm, familial atmosphere.

“We are proud that we were able to organize this year’s German-speaking AGN meeting. Our goal was to provide a personal, intimate setting where existing friendships could be strengthened, and new connections could flourish. We believe we succeeded and are already looking forward to seeing our friends again at the next meeting.”

Benjamin Block, Partner at Aeberli Treuhand AG.

A Robust Program with a Focus on Collaboration and Growth

The meeting on Friday offered participants a mix of professional workshops and engaging social activities. Highlights included:

- “Introduction to Switzerland’s Political System and Economy,” presented by Swiss National Council member Petra Gössi, offering international guests valuable insight into the Swiss landscape.

- “Staff Retention: Going a Different Way,” using Aeberli Treuhand’s innovative approaches as a case study to inspire others in the industry.

- A session on artificial intelligence, providing practical examples and applications within the industry.

- Case study: Relocation, Tax implications of moving from Germany to Switzerland in both countries – extendable to other European countries.

- “Bringing Money to Switzerland,” a presentation by representatives from Zürcher Kantonalbank, the second-largest bank in Switzerland, explaining the processes and benefits for foreign clients.

- “The Liechtenstein Foundation,” which detailed how this structure operates and the advantages it offers to international clients.

The day also included a short city tour, followed by an evening of Swiss cuisine and an after-party in the heart of Zurich, where participants continued their discussions in a relaxed and festive environment.

Andreas Weinberger from WirtschaftsTreuhand GmbH commented, “This year’s meeting brought a wonderful balance of professional insights and genuine camaraderie. Aeberli Treuhand’s hospitality and attention to detail truly made us feel at home, strengthening the collaborative spirit within our association.”

Chocolate course at Lindt

At the same time, the accompanying persons visited the famous Lindt chocolate factory. In addition to a tasty lunch, this also included a chocolate course where the participants were able to make their own chocolate creations.

The German-speaking AGN meeting at Aeberli Treuhand AG stands as a testament to the power of professional community and shared experiences. The organizers, including Susanne Cilurzo and Feri Cilurzo, both of whom played key roles in orchestrating the event’s many facets, expressed gratitude for the enthusiastic participation and are already looking forward to the next gathering.

The post Press Release: Aeberli Treuhand AG Hosts Successful German-Speaking AGN Meeting in Zurich, Switzerland appeared first on AGN International.

]]>The post The Importance of ESRS G1 Business Conduct appeared first on AGN International.

]]>ESRS G1 Business Conduct emphasizes ethical behavior, integrity, and compliance with laws and regulations in all business interactions and operations. But, how important is ESRS G1 Business Conduct in relation to other European Sustainability Reporting Standards (ESRS)?

Within the scope of the ESRS, ESRS E1 Climate Change and ESRS S1 Own Workforce are typically regarded with high importance. The question is; Should ESRS G1 Business Conduct have (at least) the same status?

Based on the alignment of ESRS G1 with crucial aspects of sustainable corporate governance and against the background of the following topics (ESRS G1.2), in my opinion, the affirmative response to this question is “yes”.

- Business ethics and culture

- Combating corruption and bribery

- Management of relations with suppliers (including payment practices)

- Lobbying activities

Overview of the ESRS G1 reporting requirements

ESRS G1 consists of two “Related to ESRS 2” disclosure requirements (GOV-1 and IRO-1) and six additional DRs. These DRs, in turn, contain 51 fundamentally reportable data points. With the exception of “Related to ESRS 2 IRO-1”, all DRs and data points are subject to materiality requirements. They are, therefore, only reportable if the related sustainability aspects have been classified as material in the materiality analysis either from the perspective of “impact materiality” and/or “financial materiality”.

“Related to ESRS 2 IRO-1” DR of ESRS G1

This disclosure requirement is considered “always mandatory” and is therefore not subject to materiality. All companies required to report in accordance with the CSRD must include the related information in their sustainability reporting. In accordance with ESRS G1.6, the procedure within the scope of the materiality analysis must be described with reference to the determination of the material effects, risks and opportunities in connection with the corporate policy (business conduct) – This also includes the disclosure of all relevant criteria used in the process.

Other key disclosure requirements of ESRS G1

In the area of corporate ethics and culture, information must be provided on how the company defines, implements and reviews its ethical principles and codes of conduct. Other key reporting requirements relate to how employee involvement and commitment is promoted and how ethical dilemmas or conflicts are dealt with. It also concerns how the fight against corruption and bribery is ensured.

With regard to relationships with suppliers, the objective of ESRS G1 is to create transparency and accountability of the reporting entity in the upstream value chain. In particular, information on the management of relationships with suppliers must be disclosed. The disclosures on the company’s payment practices, particularly with regard to late payments to small and medium-sized enterprises (SMEs), are of particular relevance from the perspective of the stakeholders concerned. Further disclosure requirements relate to the selection process of suppliers from a sustainability perspective.

The third material topic area relates to the provision of information on the following:

- Company activities and obligations related to the exercise of its political influence

- Description of the nature and purpose of any lobbying activities

- Assurance and monitoring related to compliance with applicable laws and regulations

From a lived culture of values to audit-proof governance structures

Within the scope of the ESRS G1 reporting requirements, companies can, for example, draw on existing guidelines in the procurement area and on risk and complaint management systems that have already been implemented. However, particularly in the area of owner-managed SMEs, it will also be a question of underpinning the historically grown and lived value-oriented corporate culture (in the sense of “grandfathering”) with appropriately documented and audit-proof processes and transferring them into strategic governance structures.

Should you ever lose track of the big picture, my colleagues and I from the AGN EMEA Accounting, Auditing & Education Committee (AAEC) will be happy to help and guide you safely through the IFRS and CSR jungle. As a member of AGN International, you can use the AGN AAEC Helpline at any time or contact me by email at carsten.ernst@wirtschaftstreuhand.de or by mobile phone at +49 173 8710322.

Happy accounting and stay sustainable,

Carsten

Carsten Ernst Managing Partner Wirtschafts Treuhand Group Stuttgart, Germany | – Expert in financial (IFRS) and sustainability (ESRS and GRI) reporting – Audit of financial and sustainability reports in accordance with ISAs – Member of the following AGN bodies: – EMEA Board of Directors (Chairman) – EMEA AAEC Accounting, Auditing and Education Committee (Member) |

The post The Importance of ESRS G1 Business Conduct appeared first on AGN International.

]]>The post ESRS Materiality Analysis in Medium-Sized Businesses appeared first on AGN International.

]]>The materiality analysis is the “linchpin” of future Corporate Sustainability Reporting Directive (CSRD)/European Sustainability Reporting Standards (ESRS) sustainability reporting.

The scope of the future sustainability report depends crucially on which sustainability aspects are on the so-called “material topic” list at the end of the materiality analysis. Furthermore, this list provides the basis for the development of a company-specific sustainability strategy.

Due to the complexity of the requirements of both ESRS 1 (General Requirements) and the current EFRAG draft “Materiality Assessment Implementation Guidance (MAIG)”, it is important for SMEs to implement these requirements in a pragmatic yet standard-compliant and audit-proof manner.

The Principle of Materiality

The ESRS consist of 12 standards, 82 Disclosure Requirements (DRs) and 1178 individual reporting requirements (so-called data points). So much for the bad news. The good news is that most of these reporting requirements are subject to materiality.

Only the data points that relate to the list of “material topics” must be reported on (only the DRs and data points of ESRS 2 – incl. the “related to ESRS 2 IRO-1” DRs in the topic-related standards – are considered “always mandatory”). The task of the materiality analysis is to identify these “material topics”.

From the “Long List” to the “Material Topic List

The starting point for the materiality analysis is (mandatory!) a list of the fundamentally relevant sustainability aspects (so-called “long list”), which are presented in tabular form in ESRS 1.AR.16. However, both ESRS 1 and the MAIG make it clear that this list must be adapted to include sustainability aspects specific to the industry/company.

Depending on the industry/company, the “long list” contains approximately 100 potentially relevant sustainability aspects. Examples of sustainability aspects are climate change, energy intensity, resource consumption, water consumption, appropriate remuneration, and gender equality.

As part of the materiality analysis, the “long list” is now successively shortened in several steps. In practice, a so-called “medium list” should first be derived on the basis of environmental analyses, peer group comparisons, expert surveys and the involvement of internal and external stakeholders.

The remaining sustainability aspects are then assessed and prioritized individually in accordance with the principle of dual materiality, both from the perspective of impact materiality (inside-out perspective) and financial materiality (outside-in perspective). Once a company-specific materiality threshold has been defined, the result of the materiality analysis is a list of “material topics”, usually referred to as a “short list”. This forms the basis for determining the data points to be reported in accordance with the topic-related ESRS.

Appendix E to ESRS 1 contains a “flowchart for determining disclosures under ESRS.” This shows that materiality considerations are possible at three levels:

- At the standard level: to the extent that a standard is assessed as not material, this automatically also applies to all DRs (with the exception of “related to ESRS 2 IRO-1 DRs) and data points of this standard;

- At the level of the DRs (to the extent that a DR is assessed as not material, this also automatically applies to all data points of the DR) and;

- At the level of individual data points.

Focusing On What Is Essential

There is no question about it: SMEs, in particular face major challenges in connection with first-time sustainability reporting based on the CSRD/ESRS. However, since the majority of the reporting requirements are subject to materiality, it is particularly important to identify those topics in the materiality analysis that are actually relevant for the respective company from the perspective of both “impact materiality” and/or “financial materiality”. Thus, the materiality analysis is the decisive lever for scaling the reporting obligations.

The Materiality Analysis in 6 Steps

1. Creation of the “long list“

Based on ESRS 1.AR 16. addition of industry/company-specific sustainability aspects

2. Derivation of the “medium list“

Interviewing internal and external experts, peer group comparisons, involvement of internal and external stakeholders, etc.

3. Assessment of impact materiality

Inside-out perspective

4. Assessment of financial materiality

Outside-in perspective

5. Determination of threshold value

Company-specific determination with reliable documentation

6. Finalization of the “material topic list”

If necessary, visual presentation as materiality matrix

Should you ever lose track of the big picture, my colleagues and I from the AGN EMEA Accounting, Auditing & Education Committee (AAEC) will be happy to help and guide you safely through the IFRS and CSR jungle. As a member of AGN International, you can use the AGN AAEC Helpline at any time or contact me by email at carsten.ernst@wirtschaftstreuhand.de or by mobile phone at +49 173 8710322.

Happy accounting and stay sustainable,

Carsten

Carsten Ernst Managing Partner Wirtschafts Treuhand Group Stuttgart, Germany | – Expert in financial (IFRS) and sustainability (ESRS and GRI) reporting – Audit of financial and sustainability reports in accordance with ISAs – Member of the following AGN bodies: – EMEA Board of Directors (Chairman) – EMEA AAEC Accounting, Auditing and Education Committee (Member) |

The post ESRS Materiality Analysis in Medium-Sized Businesses appeared first on AGN International.

]]>The post Is the EU Commission now “greenwashing” CSRD sustainability reporting? appeared first on AGN International.

]]>As it did with the EU Taxonomy Regulation, we question whether the EU Commission is now “greenwashing” CSRD sustainability reporting.

After the European Financial Reporting Advisory Group (EFRAG) “expert group” submitted its drafts on Set 1 of the European Sustainability Reporting Standards (hereinafter EFRAG-ESRS) to the EU Commission in November 2022, the Commission published its revised versions on June 9, 2023 (hereinafter EU-Com.-ESRS) and put them out for public consultation.

The question now arises as to whether these EU-Com.-ESRS violate the European Accounting Directive (hereinafter BilR), as amended by the Corporate Sustainability Reporting Directive (hereinafter CSRD), at least in two key points.

1. Provision of information central to allocating cash and capital flows to sustainable enterprises and business models.

According to the EFRAG ESRS, certain reporting requirements were classified as “always mandatory” according to Appendix C of ESRS 2.

“Always mandatory” means that all reporting entities must include this information in their sustainability report, regardless of whether it is considered material based on the entity-specific materiality analysis.

Sustainable Finance Disclosure Regulation:

These reporting requirements relate to information that financial market participants (especially banks) need to fulfill their own disclosure obligations based on the Sustainable Finance Disclosure Regulation (SFDR) – one of the central points of criticism of the previous practice of sustainability reporting.

The European Green Deal:

The objective of the European Green Deal is to channel money and capital flows into “green” companies and business models. With the SFDR, financial market participants were obliged to be more transparent in this respect. However, financial market participants have not been able to fulfil these obligations, as companies have not been required to disclose the necessary information – The CSRD should change this. Consequently, EFRAG has classified these reporting obligations as “always mandatory”.

EU-Com. ESRS:

However, this has not been adopted in the EU-Com. ESRS. According to EU-Com.-ESRS, this information – which is mandatory for financial market participants – is only to be disclosed if it has also been classified as material on the basis of the company-specific materiality analysis. This results from EU-Com.-ESRS 1.29, 1.33 as well as the deletion of the sentence “They are to be reported irrespective of the outcome of the materiality assessment” in EU-Com.-ESRS ESRS 1—Appendix B.

This means that companies would only have to include this information in their sustainability report if it was also classified as material on the basis of the materiality analysis (in which, as is well known, there is a great deal of scope for estimation and discretion).

EU Commission and Art. 29b (1) BilR:

The amendment made by the EU Commission is problematic, as, in my opinion, it is not in line with the following provision in Art. 29b (1) BilR: “In the (ESRS), the Commission shall (…) specify the information that companies (…) are required to report, which shall include at least the information that financial market participants subject to the disclosure requirements of the (SFDR) need in order to comply with these obligations”. The EU Commission did not observe this clear requirement of the BilR in the context of the EU Com. ESRS.

Irrespective of this potential legal violation on the part of the EU Commission against its own EU Accounting Directive, the achievement of one of the central objectives of the European Green Deal and the CSRD would not be achieved or would at least be significantly impeded: the allocation of money and capital flows to sustainable companies and business models.

2. Sustainability reporting and financial reporting at eye level versus “scattering” of sustainability information in various reports.

Sustainability and financial reporting:

The sustainability report has so far played a shadowy existence in the perception of report addressees compared to the financial report. Another objective of the CSRD is to change this in the future and to ensure that sustainability reporting is on an equal footing with financial reporting.

The new BilR:

According to the new BilR amended by the CSRD, the ESRS are to specify “what information entities (…) are required to report” (Art. 29b (1) BilR). With regard to the presentation of the sustainability report, the BilR’s requirements for the development of the ESRS are then clear: the sustainability report must be “clearly identifiable in the management report by means of a section provided for this purpose” (Art. 19a (1) or 29a (1)) – This could not be formulated any clearer.

EU Council and the EU Parliament:

Both the EU Council and the EU Parliament insisted on this clear provision in the CSRD legislative process with the following justification: “Provision is made for the disclosure of information in a clearly identifiable section in the management report, in order to facilitate the readability and identification of sustainability reporting.” This justification for the above-mentioned amendment to the BilR could not be more concise.

However, and completely surprisingly, the EU-Com. now plans that an integration or “scattering” of sustainability information in the financial report as well as in other reports should also be possible and permissible (cf. EU-Com.-ESRS 1.118).

The section “Sustainability Report” in the management report would then be degraded to a list in which only the respective passages in these reports (e.g. management report, annual financial statements, corporate governance report, remuneration report) are referenced (“incorporated by reference”).

This “incorporation by reference” would be exactly the opposite of “readability and identification of sustainability reporting” and “disclosure in a clearly identifiable section”. In my view, this would contradict the meaning and purpose of the clear requirements of the BilR – also against the background of the objective and history of the CSRD.

Missed opportunity:

Irrespective of this legal approach, the final adoption of EU-Com.-ESRS 1.118 would once again have missed the great opportunity in the implementation of the CSRD with regard to the equivalence of sustainability reporting with financial reporting (as was already the case with the predecessor directive, Non-Financial Reporting Directive (NFRD).

CONCLUSION

In relation to the two points discussed here, the EU Commission has, in my opinion, not observed the requirements of the BilR amended by the CSRD for the adoption of delegated CSRD/ESRS acts and would thus be in breach of its own BilR. In the event of final adoption by the EU Commission, the EU Council and the EU Parliament would have to fulfil their role and, in my opinion, at least raise objections in this regard.

In implementation practice, both the preparers and the auditors of sustainability reports would be faced with the question of what should now apply: the clear requirements of the Accounting Directive or the regulations of the European Sustainability Reporting Standards that deviate from them. It does not take much imagination to see that this question will probably be answered inconsistently for now.

However, it is questionable whether the EU Council and the EU Parliament should wait until the EU Commission has adopted the final ESRS before reacting. Since the EU Commission quite obviously does not adhere to the clear requirements of the CSRD (or the BilR amended by the CSRD) in the current ESRS drafts, at least with regard to the above-mentioned points (and taking into account numerous other inconsistencies in the EU Commission’s ESRS).

The question arises as to whether the EU Council and the EU Parliament should not now immediately withdraw the authority granted to the EU Commission under the CSRD to issue delegated CSRD/ESRS legal acts.

And they should do so before a comprehensive “greenwashing” of the CSRD on the basis of delegated acts of the EU Commission takes place.

Unfortunately, this has already happened with the EU Environmental Taxonomy Regulation regarding the possibility of classifying certain nuclear power and natural gas activities as environmentally sustainable economic activities. In this regard, Greenpeace, BUND, WWF and other NGOs initiated legal action against the EU Commission at the European Court of Justice in Luxembourg in April 2023: “With the decision to classify fossil natural gas as climate-friendly, the EU Commission has put itself on very thin ice, both factually and legally” (BUND Chairman Olaf Bandt).

The ice on which the EU Commission has now set itself with the classification of the sustainability information required by financial market participants as “mandatory only if material” and the option to “scatter” the sustainability information in several reports is likely to be at least as thin.

Should you ever lose track of the big picture, my colleagues and I from the AGN EMEA Accounting, Auditing & Education Committee (AAEC) will be happy to help and guide you safely through the IFRS and CSR jungle. As a member of AGN International, you can use the AGN AAEC Helpline at any time or contact me by email at carsten.ernst@wirtschaftstreuhand.de or by mobile phone at +49 173 8710322.

Happy accounting and stay sustainable,

Carsten

Carsten Ernst Managing Partner Wirtschafts Treuhand Group Stuttgart, Germany | – Expert in financial (IFRS) and sustainability (ESRS and GRI) reporting – Audit of financial and sustainability reports in accordance with ISAs – Member of the following AGN bodies: – EMEA Board of Directors (Chairman) – EMEA AAEC Accounting, Auditing and Education Committee (Member) |

The post Is the EU Commission now “greenwashing” CSRD sustainability reporting? appeared first on AGN International.

]]>The post IRS Issues Moratorium on ERC – What You Should Do Next appeared first on AGN International.

]]>On Sept. 14, 2023, the Internal Revenue Service (IRS) announced a moratorium on processing new Employee Retention Credit (ERC) claims effective Sept. 14, 2023, to Dec. 31, 2023. The moratorium comes with continued mounting concern regarding questionable ERC claims and potential scammers, as well as concerns from tax professionals. Now that the moratorium is here, what should the next move be for taxpayers who already filed their ERC claim?

Getting a Second Look for Your ERC Claim

With the heightened attention now given to ERC, IRS Commissioner Danny Werfel has recommended that taxpayers with questions or concerns about their ERC claim should immediately contact a qualified tax professional to evaluate and assess their claim validity and eligibility.

If you filed your ERC claim early before any IRS guidance was released, or you have second thoughts about the provider you used to prepare and file your claim, Windham Brannon’s Tax Controversy Practice can provide a second look of review to help you avoid being subject to additional financial impact if you do not proactively correct any errors.

During a second look review, our professionals review and verify the following information:

- Review your ERC eligibility of either your gross receipts calculation or your partial shutdown due to government mandate criteria.

- Ensure that you were appropriately deemed a small or large business employee.

- Ensure that you correctly consider your Paycheck Protection Program (PPP) loan.

- Ensure that you excluded owners and relatives from the employee calculations.

- Recalculate and file your amended return if necessary.

Key Takeaways from the New Moratorium

The following are key takeaways from the moratorium for impacted taxpayers who either already filed for their ERC claim or had planned to do so this year.

- The IRS currently has at least 600,000 ERC claims not yet processed.

- The IRS will continue to work on previously filed ERC claims received prior to Sept. 14, 2023. Refunds for previously filed ERC claims will be issued during the moratorium but at an even slower pace than before due to additional IRS review.

- Detailed compliance reviews will be implemented for ERC claims not yet issued.

- The IRS may request additional documentation from filing taxpayers before processing ERC claims.

- There may be additional new procedures added for any future ERC claims.

- The IRS issued a new Q&A guide as of Sept. 14, 2023, for updated guidance on ERC eligibility.

- A settlement program will be rolled out for any businesses that incorrectly received the ERC and must repay the amount, including any portion or commission paid to a third-party ERC promoter (typically 20 to 25 per cent). The program will allow businesses to avoid penalties and future compliance actions.

- There will be a withdrawal option available for those who have already filed but haven’t received their ERC refund. Any fraudulent claims will not be exempt from potential criminal investigation and prosecution.

- The IRS has noted repeated instances of businesses that improperly cite supply chain issues as a basis for an ERC claim when a business with those issues will very rarely meet the eligibility criteria. Under any scenario, if a business claimed the ERC earlier and the claim has not been processed or paid by the IRS, they can withdraw the claim if they now believe it was submitted improperly – even if their case is already under audit or awaiting audit. More details will be forthcoming.

A Brief History and Context

The ERC was first introduced in March 2020 via the Coronavirus Aid, Relief, and Economic Security (CARES) Act to help businesses retain and pay their employees during the COVID-19 pandemic, with employers originally eligible to receive the credit through 2021. Employers claiming the ERC were originally not allowed to also apply for Paycheck Protection Program (PPP) loans, another incentive for businesses introduced around the same time. However, the Consolidated Appropriations Act (CAA) later made changes to ERC eligibility in December 2020, including the allowance for PPP loan participants to also claim the ERC as long as they used wages not used for PPP loan forgiveness.

The CAA also increased the 2021 maximum credit amount ($7,000 per quarter), reduced the 2021 reduction in gross receipts percentage in order to qualify (20 per cent) and changed the threshold for qualifying as a 2021 large employer (500 average full-time employees).

In March 2021, the American Rescue Plan Act (ARPA) extended the ERC through Dec. 31, 2021, and also made eligibility available for certain Recovery Startup businesses and those defined as severely financially distressed employers (SFDEs). Later in 2021, the Infrastructure Act terminated ERC for wages paid in the fourth quarter of 2021 for employers that were not Recovery Startup businesses.

Concerns for ERC Filers and Tax Practitioners

The changes and amendments to ERC filing have caused confusion about how to properly claim the credit. Specifically, employers who either (1) filed very early for the ERC before relevant guidance became available or (2) filed due to government suspension mandates related to the COVID-19 pandemic could be nervous due to the recent warnings from the IRS about the validity of their ERC claim. Unfortunately, many employers do not know where to receive credible information to file their ERC claim correctly. On top of that, many small business tax practitioners who are inundated with tax preparation may also not be up to speed on ERC eligibility guidelines – therefore, such filers may have chosen to opt for third-party assistance, making them susceptible to ERC scammers.

For tax practitioners, the concerns are equally arduous. Some practitioners won’t discover that their clients filed for ERC until they receive IRS Form 1099-INT for 2023, which reports the interest earned from the ERC refund. Many practitioners also fear they will lose the client if they disclose that their ERC claim is incorrect or lacks a reasonable basis.

Other ERC Risk Factors

The following list includes specific risk factors or errors for employers who already claimed the ERC but could subsequently be subject to an IRS audit:

- You filed for ERC for Q4 2021, but your business was in operation prior to Feb. 15, 2020. (Fourth quarter 2021 ERC is only eligible for Recovery Startup businesses that started after Feb. 15, 2020).

- You filed Form 941-X, but the original Form 941 wages are not consistent with the ERC amounts claimed.

- You filed Form 941-X, and no salaries/wages deduction on your originally filed income tax return (Form 1099-MISC or NEC contractors only).

- You filed for ERC for Q4 2021, and your income tax return three-year average gross receipts were reported in excess of $1 million. (Note that a business would not be eligible as a Recovery Startup Business due to gross receipts exceeding $1 million).

- You claimed ERC based on general supply chain issues.

- The ERC amount for any employee was greater than $5,000 in 2020 or $21,000 in 2021.

In 2019, you had more than 100 average employees and claimed ERC in 2020 for all employees or had more than 500 average employees and claimed ERC in 2021 for all employees. (Note that large employers can only claim ERC for the wages paid to employers who did not work).

You filed for ERC claiming the same wages used for Paycheck Protection Program (PPP) loan forgiveness.

WINDHAM BRANNON CAN HELP

For taxpayers who filed early, have second thoughts about the provider they used or have concerns about a possible audit of their ERC claim, a second look review can proactively help you get ahead of adverse consequences in the future as well as provide peace of mind. Windham Brannon’s professionals know the ERC and can help answer questions about ERC claims that you would expect from a professional services provider.

Our Practice Leader, Tomika Bullet, has 15 years of experience with the IRS and has prepared numerous ERC claims since January 2021. For questions or more information about ERC and the current moratorium, including a second look at a previously filed ERC claim, contact Tomika Bullet. Learn more about the ERC Risk Assessment.

GEORGIA OFFICE

3630 Peachtree Road NE, Ste 600

Atlanta, GA 30326

P: 404.898.2000

TENNESSEE OFFICE

110 Somerville Avenue, Ste 266

Chattanooga, TN 37405

P: 423.708.3423

E: info@windhambrannon.com

W: https://windhambrannon.com

The post IRS Issues Moratorium on ERC – What You Should Do Next appeared first on AGN International.

]]>